by Tim Rowan | Jun 27, 2024 | CMS, Medicare Advantage

by Tim Rowan, Editor Emeritus

We have been keeping an eye on the Medicare Advantage business as the number of beneficiaries who switch exceeds fifty percent. In past reports, we have described the federal lawsuits that accuse MA insurance companies of illicitly padding revenues while illegally denying treatments that straight Medicare would have covered. (See MedPAC Exposes More Medicare Advantage Crimes – 3/20/24)

Until now, we haven’t gone into detail about those independent brokers with the continuous TV commercials every November. It turns out, they may be even more dishonest than the insurance companies themselves.

Perhaps the most famous of these brokers is the one that put Broadway Joe Namath in our living rooms a hundred times a day. The company started life as Health Insurance Innovations, owned by Chicago-based private equity firm Madison Dearborn Partners. After accusations of fraud, the company folded and re-emerged as Benefytt. When the same accusations returned, the owners shut that company down and came back as Blue Lantern Health.

According to Healthcare Uncovered, the firm filed for a state-level bankruptcy equivalent in Delaware last April, called “assignment for the benefit of creditors.” Blue Lantern’s website is down, as are MedicareCoverageHelpline.com and HealthInsurance.com, their signature assets. Nobody answers the 800 number Namath hocked for years.

The bankruptcy litigation revealed a database of 7 million seniors who had been bombarded by 17 million phone calls. The bankruptcy was apparently precipitated by the Federal Trade Commission, which forced Benefytt to pay $100 million to the people it had scammed by selling sham Obamacare plans, with checks distributed to victims in March. The Securities and Exchange Commission forced Health Insurance Innovations and the company’s co-founder Gavin Southwell to pay a $12 million settlement. Another close associate of the company, Steven Dorfman, was convicted of wire fraud in February.

Tolerance for the firm’s deceptive advertising scheme ended with changes to the Medicare Advantage rule in 2023 that took effect in 2024. Blue Lantern stated after the fines were imposed that the new rule was critical to the company’s downfall,

Previously, former HHS Security Alex Azar characterized the Namath ads as “real savings, real options” in Medicare Advantage, ignoring the studies showing that the MA program costs the Trust Fund not less but $140 billion more than original Medicare.

Healthcare Uncovered concluded with this observation, “Further rules imposed since then by the Biden administration are putting even more pressure on Medicare Advantage lead generators, also called ‘third-party marketing organizations.’ (TPMOs) Beginning October 1 of this year, CMS will require that TPMOs get express consent from individuals before selling contact information to other marketers and brokers — a key loophole that enabled the growth of Blue Lantern and its predecessors.”

Don’t worry about Joe Namath’s retirement income though.

He has already landed a gig hawking hearing aids.

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim@RowanResources.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report. One copy may be printed for personal use: further reproduction by permission only. editor@therowanreport.com

by Kristin Rowan | Jun 13, 2024 | Clinical

by Kristin Rowan, Editor

The Home Health Value-Based Purchasing (HHVBP) Model began in 2016 as part of the Home Health Prospective Payment System (HH PPS) final rule. The original model aimed to:

- Incentivize better quality and more efficient care

- Study potential quality and efficiency measures

- Enhance the public reporting process

The original model had an average 4.6 percent improvement in Total Performance Scores (TPS). The model also saved Medicare $141 million annually, on average. There were no adverse risks with these savings.

Additionally, the model reduced the number of unplanned hospitalizations and stays at Skilled Nursing Facilities (SNF). This provided additional savings from lower inpatient and SNF spending.

The HHVBP model expanded in 2022. The model includes HHAs in all 50 states, D.C., and the U.S. territories. The model adjusts Medicare payments from the fee-for-service (FFS) model. Quality measures in a Performance Year impact adjustments in the Payment Year. These adjustments range from -5% to 5% and are based on quality measures relative to peer performance. HHA peers are pre-assigned cohorts with HHAs of similar size.

The expanded HHVBP model uses data from the Home Health Quality Reporting Program (HH QRP), Medicare claims, and HHCAHPS surveys. The expanded model does not require any additional data at this time.

Additional information on the quality measures, cohorts, guides, and recordings from CMS can be found here.

We will continue to follow this story and provide updates on the new expanded model as they come in.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report. One copy may be printed for personal use: further reproduction by permission only. editor@therowanreport.com

by Rowan Report | Apr 26, 2024 | Admin, Clinical, CMS, Regulatory

by Johnathan Eaves, Senior Director of Communications, Axxess

Treating Medicare patients comes with a level of nuance that is important to understand to ensure that organizations remain compliant and patients receive appropriate care. Standards for quality care and payment can sometimes be dictated by Medicare’s payment policies and at other times be decided by the Conditions of Participation. There is an important difference between these two governing principles that providers should understand to ensure compliance.

Care at home industry veteran and Axxess Senior Vice President of Clinical Services Arlene Maxim RN, HCS-C, offered insights into the differences between Medicare’s policy and its Conditions of Participation during a recent webinar.

Explaining the Difference

Maxim pointed out that the differences between policy and the conditional requirements comes down to what can be billed and what are the quality standards for the services provided.

“The Conditions of Participation are dealing primarily with quality, whereas Medicare policy is related to payment,” said Maxim. And while there is a difference, that doesn’t mean both aren’t important and must always be followed.

“If Medicare policies are not followed, you are audited and if you do not have documentation to support those policies, you’re not going to get paid,” said Maxim “Oftentimes, with PDGM, staff members are not getting past that first 30 days. They’re not understanding what they need to do to keep that patient who continues to qualify for services on for longer.”

Maxim says that the problem is often that clinicians do not understand Medicare policy. “Every piece of documentation we submit to the Medicare program for review [needs to be] as pristine as we can possibly get it,” she said.

Assessment and Documentation

Proper assessment and documentation is something Maxim feels is critical in ensuring quality care, meeting Medicare requirements, and receiving payment for services.

“Complete and detailed documentation is going to be the key for agency payment by the Medicare program,” Maxim said.

Maxim pointed out certain services covered under Medicare policy may include observation and assessment, management and evaluation of a care plan, maintenance therapy, teaching and training activities, administration of medications, wound care, ostomy care, rehab nursing, venipuncture, skilled nursing visits, and more.

She also cautioned that agencies need to be prudent with the funds they receive from Medicare, viewing them as a potential “short-term, interest-free loan” until undergoing any audit. Until their documentation is reviewed and approved, there are no guarantees.

“Medicare is an insurance and it’s not free,” said Maxim. “Medicare policy provides us with a list of covered items. If experiencing an audit, and if the documentation is not there to cover the covered service, you’re not in compliance with that Medicare policy and you will not be paid for the services.”

Communicating With Physicians

Maxim further emphasized the importance of frequent contact with physicians, adherence to care plans, and ensuring that care plans are simple with individualized plans and goals that are achievable.

“You want to make sure that you have orders that physicians are actually going to read and to determine that they make sense and they’re going to sign off on them,” said Maxim.

“Keep your plan of care simple.”

# # #

Axxess Home Health, a cloud-based home health software, streamlines operations for every department while improving patient outcomes.

© 2024 Axxess. For reprint permission, please contact The Rowan Report: kristin@therowanreport.com

by Rowan Report | Apr 26, 2024 | CMS, Medicare Advantage, Regulatory

By Beth Noyce, RN, BSJMC, BCHH-C, COQS

CHAP-certified home health & hospice consultant

This is part 3 of the 3 in the series, outlining the discussions and implications in adopting new outcome and process measures for Hospice care. The final segment addresses future process and outcome measures that the board discussed, but did not yet implement. Read Part 1 on Outcome Measures and Part 2 on Process Measures.

The TEP discussed potential future process and outcome measure concepts that Abt Associates presented to the panel as well.

The process measures included:

- Education for Medication Management

- Wound Management Addressed in Plan of Care

- Transfer of Health Information to Subsequent Provider

- Transfer of Health Information to Patient/Family Caregiver

Hope-based outcome measures were:

- Patient Preferences Followed throughout Hospice Stay

- Hospitalization of Persons with Do-Not-Hospitalize Order

Developing education for medication management as a process measure was a popular concept, and the top priority of the recommended measures with the TEP as they “broadly agreed that CMS should develop this measure,” the report says, citing “a significant need for training in medication management for patients and their caregivers.” They recommended that the measure weigh more heavily when care is provided in a home setting than in a facility setting because hospices are unable to control facility training and hiring practices. One panelist commented that including the phrase “during today’s visit” in the measure is important.

Whether CMS should further develop the process measure addressing wound management in the plan of care was less straight-forward, as panelists provided varied feedback. They generally agreed that this measure is important, as having a record of wound management addressed in the plan of care can hold the staff accountable for treating the wounds. But some members recommended measuring wound management with outcome measures rather than process measures. One panelist cited potential problems from patients’ deterioration over time and another noted that the time frame of this measure is important, and encouraged recording the process of getting care in place once a wound is identified. The panel agreed CMS should carefully define the measure’s specifications.

Because standard practice for most agencies is, when a patient is discharged live, to transfer health information to the subsequent provider and to the patient and family or caregiver, TEP members expressed that the two measures were likely to “top out,” meaning they would almost always be marked “Yes,” making them of no value in differentiating between hospice providers. The group generally discouraged developing these process measures.

The group strongly rejected any merit in developing two outcome measures concerning Patient Preferences Followed Throughout Hospice Stay and Hospitalization of Persons with Do-Not-

Hospitalize Order. The report says “Multiple TEP members described situations in which patients who had preferred not to be hospitalized changed their minds when a crisis occurred. Patients’ preferences and unexpected crises are usually out of the hospice’s control. Although it is still important for hospices to ask patients about their preferences as part of patient-centered care, the TEP did not believe these two items would be practical measures of a hospice’s care quality.”

Dr. McNally expects that Abt. Associates will apply the HQEP TEP’s suggestions to the HOPE tool.

“Oh yeah, they did it,” he says. “Abt would come to a specific meeting with information, data, suggestions, and specific information about how these things would be measured. We’d give feedback. Then they’d come back to the next meeting having incorporated our suggestions,” he explains. “All of us felt very much heard and responded to. It didn’t feel in the least bit perfunctory.”

Whatever specific measures are eventually included in the HOPE tool, Lund Person sees value in its implementation. “Hospice providers have had a woeful lack of outcome measures for hospice patients, which has made the evaluation of quality hospice care based only on process measures and the family’s evaluation of hospice care in the CAHPS® Hospice Survey, she explains. “Implementing HOPE will begin to identify outcome measures that can be compared between providers.”

Lund Person warns of potential challenges as well. “The selection of risk adjustment and stratification must be carefully done to minimize bias and maximize effectiveness of measures,” she says. “In addition, hospice providers have been awaiting the release of the HOPE tool with significant anxiety about content and administrative burden.”

Dr. McNally is confident the HOPE tool will be a healthy change for hospices.

“A lot of my role as a medical director and hospice physician is supporting our nurses,” he says. “They do 95% of the work. I really would like to see this not be burdensome for our hospice nurses. I’m looking forward to seeing what the [HOPE tool] beta testing translates to in our own hospice world.” He added “What I would hope to see is that the tool feels user-friendly to the hospice team, the people who have to use it, and that it also provides useful information to patients and families.”

NAHC’s Wehri says that standardizing processes through the HOPE tool is the key foundational element for the hospice industry. “High quality care is driven by reducing variance through standardized processes, Wehri writes. “Also, CMS will have a better idea of how the type of population a hospice serves impacts some of the clinical care.” This small glimpse into hospice variances that CMS does not currently have could be very helpful in future policy and payment decisions, according to Wehri. “What CMS finds in terms of differences between hospices and their care for patients may be a bit of a surprise to CMS,” she says. “I hope they are pleasantly surprised with the overall quality of care that is revealed.”

# # #

Beth Noyce provides education, consulting, mentoring, compliance assessments and auditing services to home health and hospice agencies and their clinicians in several states. She also now provides patient and family guidance concerning hospice and home health services. Beth loves teaching and helping others succeed. She also makes available recordings of much of her education for her clients’ convenience.

Beth Noyce provides education, consulting, mentoring, compliance assessments and auditing services to home health and hospice agencies and their clinicians in several states. She also now provides patient and family guidance concerning hospice and home health services. Beth loves teaching and helping others succeed. She also makes available recordings of much of her education for her clients’ convenience.

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report. One copy may be printed for personal use: further reproduction by permission only. editor@therowanreport.com

by Tim Rowan | Mar 20, 2024 | CMS, Editorial

by Tim Rowan, Editor Emeritus

This week, we look at the state of the healthcare industry, vis a vis payers that do not pay.

While Home Health and Hospice leaders talk at every gathering about refusing to accept Medicare Advantage clients, some large Integrated Healthcare Systems are actually doing it. Other hospitals are responding to difficult payers by laying off staff, or even closing. The HHS Office of Inspector General repeatedly fines insurance companies for upcoding to gain inflated, unjustified monthly payments. Meanwhile, insurance companies report record profits, with their MA divisions leading the way. The fines go into the “cost of doing business” column.

March, 2024, Becker’s Hospital Review: Bristol (Conn.) Health will eliminate 60 positions, 21 of which are currently occupied and will result in layoffs at Bristol Hospital. The hospital’s CEO, Kurt Barwis, told a local newspaper a lack of reimbursement from insurers left the hospital without a choice but to cut staff.

October, 2023, NPR: Since 2010, 150 rural hospitals have closed. Under CMS’s “Critical Access” designation, Medicare pays extra to those hospitals to compensate for low patient volumes. MA plans do not. Instead, they offer negotiated rates that are lower than what traditional Medicare would pay.

December, 2023, Becker’s Financial Management: 13 additional hospital systems cut ties with Medicare Advantage plans since October.

What is going on?

The Medicare Payment Advisory Commission, MedPAC, believes it has learned the answer. In its March 15, 2024 report to Congress, the Commission called for a “major overhaul” of Medicare Advantage policies. It says it found that the program, designed to lower costs and extend the lifespan of the Medicare trust fund, does not save money but costs the fund more than if all beneficiaries were on traditional Medicare, $83 billion more in 2024.

Calling it, too politely, “coding intensity,” MedPAC concurs with the OIG that MA plans routinely exaggerate patient conditions. The report claims it will amount to MA clients appearing to need 20% more healthcare than fee-for-service beneficiaries, when they do not. Padded coding, MedPAC says, will increase Medicare premiums by $13 billion in 2024.

“A major overhaul of MA policies is urgently needed for several reasons,” the commission wrote in its report. MedPAC cited several problems that need to be addressed, including the disparity in costs between beneficiaries in fee-for-service Medicare and MA, a lack of information on the use and value of supplemental benefits, and challenges setting benchmark payment rates.

A proposal currently making its way through Congress would reduce supplemental payments to insurers, who threaten to raise premiums and cut benefits if their inflated benchmark payments are lowered.

“If payments to MA plans were lowered, plans might reduce the supplemental benefits they offer,” MedPAC wrote in its report. “However, because plans use these benefits to attract enrollees, they might respond instead by modifying other aspects of their bids.” The barrage of TV ads, featuring aging celebrities, have been found to be deceptive and too often backed by shady front companies representing brokers, not insurance companies. The brokerage company behind the Joe Namath ads, for example, has reorganized and changed its name three times.

Pushback from AHIP, the insurance industry lobbying organization, has been as expected. “MedPAC’s estimates are based on ‘speculative assumptions’ and ‘overlook basic facts about who Medicare Advantage serves and the value the program provides.'”

MedPAC asserts that its estimates are based on history, not speculation.

Healthcare Providers Beg to Differ

A lack of payments from Medicare Advantage plans is one reason the Connecticut hospital is laying off staff, the Hartford Courant reported March 14. CEO Kurt Barwis told the newspaper Medicare Advantage plans have been denying claims more frequently while delaying payments for the claims they do approve. “Our primary care is to take care of patients, their single focus is shareholder value and profits,” Mr. Barwis told the Courant. “The Medicare Advantage abuse is outrageous.”

The strategy insurance companies deploy to avoid providing care, Barwis continued, is excessive prior authorizations, coupled with delayed payments. This obstacle to care is directly in opposition to CMS policy. MA divisions of large insurers respond that they are private insurance and allowed to impose their own treatment approval policies. MedPAC says this claim is incorrect.

Richard Kronick, a former federal health policy researcher and a professor at the University of California-San Diego, said his analysis of newly released Medicare Advantage billing data estimates that Medicare overpaid the private health plans by more than $106 billion from 2010 through 2019 because of the way the private plans charge for sicker patients. Kronick added that there is “little evidence” that MA enrollees are sicker than the average senior, though risk scores in 2019 were 19 percent higher in MA plans than in original Medicare. That gap continues to widen.

Where does this excess taxpayer money go?

2023 Medicare Advantage business division profits and 2022 CEO compensation reported by publicly traded companies:

UnitedHealth Group: $22.4 B (Andrew Witty $20,865,106)

Aetna (CVS): $8.3 B (Karen Lynch $21,317,055)

Elevance Health (Anthem): $6 B (Gail Boudreaux $20,931,081)

Cigna: $5.1 B (David Cordani $20,965,504)

Centene: $2.7 B (Sarah London $13,246,447)

Humana: $2.5 B (Bruce Broussard $17,198,844)

We found one curious outlier. Molina Health, with annual revenue 10 percent of UnitedHealth Group’s income and 2.16 percent of the market, paid its CEO $22,131,256 in 2022.

Download the entire MedPAC 2024 report here. Chapter 7 is the Home Health section. A summary of MedPACs recommendations begins the chapter thus, “For calendar year 2025, the Congress should reduce the 2024 Medicare base payment rates for home health agencies by 7 percent.”

# # #

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim@RowanResources.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Kristin Rowan | Feb 7, 2024 | Admin, Marketing, Regulatory

by Kristin Rowan, Editor

Medicare Advantage has multiple measures of success for payment bumps and bonuses. Rehospitalization rates has long been the most important measure of how well a care at home agency is performing, but there are additional measures that can help or hurt your agency. One that is gaining a lot of traction with MA and can impact your agency’s ability to survive is the overall patient experience. Measuring the patient experience can be subjective, but a great marketing tool to use is the Net Promoter Score (NPS). NPS is a calculation of patient responses regarding their likelihood to recommend you to others. A NPS score of “0” means that, overall, your clients are not going to speak positively or negatively about you; there just isn’t anything outstanding enough to bother saying anything. Anything above zero is better than nothing, but 30 and above is ideal.

During January’s HomeCare 100 Winter Conference, Tim Craig moderated the panel, “The MA Member Experience and Why it Matters” with a panel of experts. He posed this question to the audience:

“How well do home care providers perform when it comes to delivering on patient experience?”

Rating care provider performance on a scale of 1-5, the responses during the panel were somewhat surprising

- 47% of those who responded rated the delivery on patient experience 3

- 43% said 4

- 6% responded 2

- A mere 4% responded 5

- There were no responses of 1

If we turn these answers into a Net Promoter Score, we get -6. If caregivers, administrators, and providers don’t believe we’re doing a good job, how can we expect our clients, patients, and families to be happy with the care they receive?

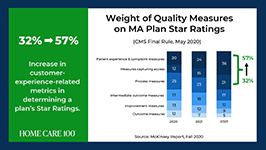

Statistics

- Patient experience and complaint measures count higher toward star rating than they have before

- CAHPS Scores have changed weight from 1.5 to 4 since 2021

- Star Ratings Determine Bonus Eligibility and Amount – starts at 4 stars and above

- Number of plans that have a 4.0 or higher star rating dropped from 64% to 43%

- Disenrollment is on the rise from 10% in 2017 to 17% in 2021

Net Promoter Score

Glen Moller, CEO of Upward Health, whose net promoter score is a whopping 86, said:

“The Member Experience has always been important. What has changed is the way we manage it, given the implication of the CAHPS rating, you can’t be a 4 star without high CAHPS scores.” Moller improved his patient experience with internal surveys to get actionable intel and asking open-ended questions. Look at change and innovation and how that could be disruptive to members. Member experience is at the center of all the other measures. No matter what benefits you’re offering, embed member experience measures at every step of the process.

Because your star rating directly impacts your ability to receive bonuses and because experience-related metrics are increasingly weighted in determining star ratings, you should be looking at the member experience more closely in all of your process. You should also be measuring the member experience and looking at ways to improve it.

Ways to measure ME

• HHCAHPS

• Quality of Patient Care Ratings

• Word of Mouth

• Net Promoter Score

• Glassdoor

• YelpCalculating a Net Promoter Score can be challenging, especially when trying to get older or infirmed patients to answer a survey. For the most accurate NPS, send a single question survey to all of your current and past customers asking them to rate, on a scale of 1 to 10, “How likely are you to recommend us to a friend or family member.” If you aren’t able to do this, you can still calculate a rough NPS using your other measures. You can use your Google and Yelp reviews with a simple formula: % of promoters – % of detractors = NPS. Three stars and below are detractors; four and five stars are promoters.The NPS score is more about comparative to the usual experience rather then the actual experience. A high score from a customer doesn’t necessarily meant it’s “great”, only that it’s much better than what they’re used to or what they expected.

The NPS is not the only measure of customer experience. To get the whole picture, use all the data you have to find out what interventions should be done and implement them. Whether the change is in training your staff, updating your scheduling process, using AI to help communicate directly with patients and families, or simply streamlining your website for a better user experience, you can improve your chances for higher ratings and bigger bonuses in a few easy steps.

I won’t often insert a shameless plug into an article, but if increasing patient satisfaction and member experience can help your agency survive the CMS pay cuts, and you need help with getting a NPS, understanding how to measure your patient experience, or getting online reviews, please contact me for more information. My marketing agency is happy to help get you started.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Kristin Rowan | Feb 7, 2024 | Regulatory

by Kristin Rowan, Editor,

On Wednesday, January 31, Cigna and HCSC signed an agreement to sell all of Cigna’s Medicare business — including traditional Medicare, supplemental benefits, Medicare Part D offerings, and CareAllies, a value-based care management subsidiary. — to HCSC, a Blue Cross / Blue Shield partner with operations in Illinois, Texas, New Mexico, Oklahoma and Montana. The $3.3 billion deal will quadruple the size of HCSC’s Medicare Advantage population, which numbered 217,623 as of this month.

Medicare Advantage had not been a significant business for Cigna. CEO David Cordani explained that it required resources disproportionate to its size in the company. With 19 million insurance customers, Cigna had a little over a half million in its MA business, a little under a half million Medicare supplement members, and 2.5 million in Part D.

It had previously been reported that Cigna believed divesting its Medicare business would make its merger with Humana more acceptable to regulators. The company completed its HCSC deal even though negotiations with Humana had already broken down. Though inked today, the deal is not expected to close until the first quarter of 2025.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Tim Rowan | Jan 24, 2024 | Regulatory

Untitled Document

Analysis by Tim Rowan, Editor Emeritus

P

erennial Home Health enemy MedPAC angered a different group last week by releasing a status report on insurance companies participating in the Medicare Advantage program.1

The report details the way in which giant, for-profit, health insurance companies improperly increase per-customer payments by upcoding their health assessment at enrollment, and then slash costs by denying coverage for healthcare services that traditional Medicare would have honored. MedPAC was also critical of the practice of requiring prior authorizations, backed up by utilization review algorithms that are supposedly intended to “minimize furnishing unnecessary services” but which effectively increase denials for necessary care.

According to the report, MedPAC expects CMS to pay MA plans $88 billion in 2024.

On January 12, a meeting to discuss the report ended in what one reporter politely described as “a kerfuffle.” Other witnesses to the meeting chose to describe it as a shouting match.

“One member, Brian Miller, MD, MPH, of Johns Hopkins University in Baltimore, accused panel leadership of issuing a negative status report on MA plans’ market dominance, saying it had been ‘hijacked for partisan political aims to justify a rate cut to Medicare Advantage plans.’

“Miller said the analysis … ‘appears to be slanted to arrive at a foregone conclusion in order to set up and provide political cover’ just before the Centers for Medicare & Medicaid Services prepares its annual rate notice for MA plans, expected in coming weeks. ‘The chapter reads like attack journalism as opposed to balanced and thoughtful policy research.'”2

Report authors fired back, citing numerous ways MA plans generate higher revenue, including enrolling people who are relatively healthy, known as favorable selection. They then vigorously scan patients’ medical histories and charts to code for health factors that generate higher per-capita payments, known as coding intensity, often spending less on services. Coding intensity is also the difference between a risk score that a beneficiary would receive in an MA plan versus in fee-for-service. Though MA plans skew toward healthier enrollees, MedPAC found that MA risk scores are about 20.1% higher than scores would be for the same beneficiaries had they enrolled in Fee For Service Medicare.

Namath, Walker, Shatner and Brokers

Criticism of MA plan behavior did not only come from MedPAC commissioners and report authors. For example, Lynn Barr, MPH, founder of Caravan Health, which was acquired by CVS Health through its acquisition of Signify Health, exposed what the annual TV ads do not make clear, that their 800 numbers go to brokers, not to any one plan.

“This is not the big, lovely, glowing success that everybody says it is. And we continue to create policies that drive people into these plans. Medicare allows money paid to MA plans to be used for broker commissions as high as “$600 to recruit them, plus $300 a year every year that they stay in the MA plan.

“We have allowed MA to buy the market, and that is why MA is growing. It’s not because the quality’s so great. People don’t love the prior auth, people are leaving their plans a lot. Aside from Medicaid, Medicare is the least profitable payer for doctors. And at the same time, we give all this money to the plans. It’s unconscionable.”

Adding to the “kerfuffle” with a powerful anecdote, Stacie Dusetzina, PhD, of Vanderbilt University Medical Center in Nashville, Tennessee, noted that even cancer patients often have trouble getting necessary care because of the plans’ limited networks. She referenced a January 7 NPR story3 about an MA enrollee who could not get the cancer care he needed from his MA plan, and could not get out of the plan without facing 20% in expensive copays. In all but four states, supplemental plans that could pick up the difference can reject patients with costly conditions.

“When you are 65 and aging into the program,” Dr. Dusetzina summarized, “you are healthy at that time and may not be thinking about your long-term needs. [If you did], it would push you to think harder about the specialty networks that you may or may not have access to when the MA plan is making your healthcare decisions.”

1 A 30-page slide presentation is available to the public at medpac.gov/wp-content/uploads/2023/10/MedPAC-MA-status-report-Jan-2024.pdf. The complete report is available only to MedPAC commissioners. The charts on slides 26 and 27 show how MA plans learned to pad profits in 2018 and increased the practices exponentially since then.

2 Cheryl Clark, MedPage Today January 16, 2024 medpagetoday.com/special-reports/features/108275

3 npr.org/2024/01/07/1223353604/older-americans-say-they-feel-trapped-in-medicare-advantage-plans

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. RowanResources.com; Tim@RowanResources.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Tim Rowan | Dec 6, 2023 | CMS, Regulatory

by Tim Rowan, Editor Emeritus

MA Plans Continue to Exaggerate Patient Conditions for Profit

As we reported in October (More MA Plans Caught Inflating Patient Assessments, 10/11/23), insurance companies operating Medicare Advantage plans routinely pad the patient assessments that set their monthly revenue from the Medicare Trust Fund. Worse, CMS bowed to industry pressure earlier this year and agreed not to extrapolate the amount of the fraudulent payments, as it does with Home Health and Hospice overpayments (Government Lets Health Plans That Ripped Off Medicare Keep the Money, 2/22/23).

Now, we hear that the HHS OIG has totaled its 2023 audits and announced it found over $213 million in padded Medicare Advantage overpayments so far this year. In its latest semiannual report, covering fraudulent patient assessments between April and September, the OIG said it recovered $82.7 million. Total recoveries would have been higher except for that CMS ruling that prevents the agency from extrapolating payments before contract year 2018.

Will SEC Allow Cigna/Humana Marriage?

Early last month, Bloomberg broke the news that Cigna was in talks to sell its Medicare Advantage business to Health Care Service Corporation, the parent company of BCBS in Illinois, Texas, New Mexico, Montana and Oklahoma. Should that sale be approved, it would remove an obstacle to Cigna’s rumored desire to merge with Humana.

Though approval is uncertain — the SEC has squashed more than one similar attempt under both the current and former Presidents — it would create what Axios called “another Titan” that would rival UnitedHealth Group and CVS Health in size. CVS acquired Aetna in 2018. It would also combine two Pharmacy Benefit Managers, giving the new entity control of a third of the market, which would be equal to the market share owned today by CVS.

In 2017, a proposed merger between Cigna and Elevance Health, formerly Anthem, was struck down in court. A proposed merger between Humana and Aetna was also canceled in a federal court the same year. Large, powerful insurers, and the PBMs they own, have come under increased scrutiny from federal regulators.

The Biden administration has already launched a warning shot, indicating it will be scrutinizing private equity acquisitions in health care. In September, the Federal Trade Commission sued private equity firm Welsh, Carson, Anderson & Stowe after it bought up nearly all of the anesthesiology practices in Texas and then, with competition removed, began to jack up prices. FTC chair Lina Khan made it clear the suit was intended to send a message to all consolidation attempts that might harm patients.

United to Change Prior Authorization Policy

According to a November 27 policy update from UnitedHealthcare (UHC), the payer is updating its Home Health prior authorization and concurrent review process for services that are delegated to Home & Community Care, the payer’s home care division.

The updated policy, which are set to take effect January 1, will affect United’s Medicare Advantage and Dual Special Needs plans in 37 states, a UnitedHealthcare news release stated.

In Summary

- Start of care visits still do not require prior authorization.

- Providers must notify Home & Community Care of the initiation of home care services. UHC encourages providing notice within five days after the start of a care visit to help avoid potential payment delays.

- Before the 30th day, providers must request prior authorization for days 30 to 60, by discipline, and provide documentation to Home & Community Care.

- For each subsequent 60-day period, providers must request prior authorization, by discipline, and provide documentation to Home & Community Care during the 56- to 60-day recertification window.

UHC says it will respond to questions about the prior authorization approval process at HHinfo@optum.com

In related news, in its annual investor conference call, the company projected “revenues of $400 billion to $403 billion, net earnings of $26.20 to $26.70 per share and adjusted net earnings of $27.50 to $28.00 per share” for 2024. Cash flows from operations are expected to range from $30 billion to $31 billion.

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim@RowanResources.com

©2023 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report. homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Kristin Rowan | Sep 13, 2023 | Editorial, M&A, Regulatory

UnitedHealth Group Makes Bid to Buy Amedisys after Acquiring LHC Group

Amedisys is one of the leading providers of home health, hospice, and other healthcare at home services. It operates more than 500 locations in 37 states and the District of Columbia. After acquiring Contessa Health in 2021 for $250 million, Amedisys added hospital-at-home, SNF-at-home, and palliative care to its list of services.

Optum Outbids Option Care Health

In May of this year, Option Care Health and Amedisys issued joint statements announcing a merger of the two companies in an all stock-option bid. Option Care Health provides home and alternate site infusion services, while Amedisys provides home health, hospice, and high-acuity care. The merger was valued at $3.6 billion. It would have increased stockholder value, increased access to care across the United States, and created a network of more than 16,000 health care professionals, according to the joint statement.1

By June 26th, Option Care Health confirmed the termination of the merger and a $106 million termination payment from Amedisys, after Amedisys accepted an all-cash bid from UnitedHealth Group.2

UnitedHealth Expanding Service Options

UnitedHealth Group acquired LHC Group earlier this year for $5.4 billion.3 That acquisition folded LHC Group into UnitedHealth Group’s Optum. The acquisition came after increased demands for home care services. UnitedHealth Group considered this a move toward value-based care. The Federal Trade Commission stalled the merger with requests for additional details in mid-2022. Despite the FTC probe and a shareholder lawsuit, the deal was ultimately approved and the LHC Group delisted its stock on February 22.4

New Merger Faces Federal Scrutiny

Optum and Amedysis expected concerns over anti-trust issues surrounding the merger, according to a joint statement from the two groups. The Department of Justice recently asked for more information.5 The request will push back the timeline for the merger. Amedisys believes there is little geographic overlap between Amedisys and LHC Group and that the scrutiny is a result of other UnitedHealth Group acquisitions.

In a press release about the merger, Optum CEO Patrick Conway, M.D. said, “Amedisys’ commitment to quality and care innovation within the home, and the patient-first culture of its people, combined with Optum’s deep value-based care expertise can drive meaningful improvement in the health outcomes and experiences of more patients at lower costs, leading to continued growth.”6

Even with the recent acquisitions and mergers, if this deal with Amedisys proceeds, Optum will have only a 10% market share across the U.S. For this reason, as well as the demand for home care far exceeding the supply, Optum believes this merger will be approved.

Should a company that brokers health insurance also be allowed to be the provider of care? In this author’s experience, job-based healthcare insurance does not come with many options. There may be different levels of care to fit your budget, but the insurance company is already chosen by the employer. This means that employees and their families choose to have health insurance or not but cannot choose the insurance company.

Home Care, Hospice, Post-Acute Care, Palliative Care, and other in-home services are very personal. The company you choose and the care provider you get have to fit your needs and personality and there is a high level of trust needed to allow a stranger into your home when you are in a vulnerable state. If the insurance company is also providing the care, the option to find a care provider that suits the level of trust needed almost disappears.

In 2021, President Joe Biden signed an executive order for more vigorous oversight of the healthcare market. Mergers and acquisitions are being scrutinized more heavily to preclude monopolies of care. The FTC and DOJ, in response to this executive order, have proposed updates to antitrust guidelines that will make healthcare mergers and acquisitions more difficult.7

Medicare beneficiaries enrolled in Medicare Advantage has now reached 50%, making insurance companies more involved in senior care than ever before.8 Insurance companies only recently increased the percentage of revenue spent on patient care to 80%, up from as low as 50% before 2010.9 Given these facts, it may be worth questioning whether the insurance companies have too much control over care now, and if the acquisition of care providers by insurance providers should be eliminated completely to avoid a complete takeover of healthcare by insurance companies that already focus more on profit than people.

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report. One copy may be printed for personal use: further reproduction by permission only. editor@therowanreport.com