by Kristin Rowan | Feb 14, 2024 | CMS, Regulatory

By Kristin Rowan, Editor

Republican and Democratic leaders joined forces to introduce the Credit for Caring Act (S. 3702, H.R. 7165) in support of family caregivers across the country. Family caregivers are those who are caring for a family member but are not nurses or employees of any home care agency. They are not eligible for Medicare or Medicaid payments, nor is there an employer paying them for the endless hours of support they provide. Family caregivers are often under a lot of emotional and financial stress. Some have full-time jobs in addition to the care provide. Others are caring for more than one family member, sometimes in different homes.

The Credit for Caring Act, a bipartisan effort to recognize the personal cost to family caregivers with a $5,000 federal tax credit for eligible working family caregivers. As is generally the case with government intercession, the “eligible” part will exclude many family caregivers. From Congress.gov:

“This bill allows an eligible caregiver a tax credit of up to $5,000 for 30% of the cost of long-term care expenses that exceed $2,000 in a taxable year. The bill defines eligible caregiver as an individual who has earned income for the taxable year in excess of $7,500 and pays or incurs expenses for providing care to a spouse or other dependent relative with long-term care needs.”

The bill also includes the caveat that eligible caregivers must incur qualified expenses, limited to goods, services, and supports. The language excludes the time and energy a family caregiver expends, essentially limiting the tax credit to repayment of money paid out of pocket for care that should have been covered by Medicare, Medicaid, or private health insurance, but isn’t. The cost of a direct care giver is included in eligible expenses, but doesn’t consider the family caregiver to be one.

As I break down the math in my head, I come up with this:

A tax credit of $5,000 is received if the caregiver has spent $16,600 in the previous year (5,000/.3). This leaves a total out of pocket amount of $11,100. Supportive home care services average $30/hour. $16,660 is equivalent to 555 hours of non-medical home care. That’s roughly 10 hours per week or 1-1/2 hours per day. This doesn’t include the costs for DME, doctor visits, lost wages from time off work, medication, or any of the other eligible expenses included in the bill.

This is getting us one step closer to paying for supportive in-home care and palliative care services, but I don’t think it goes far enough. An under-served, under-paid population who makes $7,500 per year cannot afford $16,000 in out-of-pocket expenses in order to qualify for the maximum tax credit. Once this bill is (hopefully) passed, we should move on to including additional services in the Medicare/Medicaid reimbursement model. The Rowan Report joins NAHC in its support of the Credit for Caring Act and urges you to reach out to your representatives to urge them to support the passing of the bill.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

Read the article and statement from NAHC here

Read the full text of the bills: H.R. 3321 and S. 3702

Find your Senator here

Find your Representative here

by Kristin Rowan | Feb 14, 2024 | Admin, M&A

By Kristin Rowan, Editor

Home care is no stranger to mergers and acquisitions. It seems there is news almost daily about companies joining forces or selling parts of their company to new entities. Notably, we reported just last week that Cigna has dropped its entire Medicare Advantage book of business. This week, we have two M&A stories to share with you.

Acquisition

Texas-based agency Angels of Care, previously of Varsity Healthcare Partners, has been bought by Nautic Partners, a private equity company. Angels of Care provides pediatric home health, including private duty and skilled nursing services, along with physical and speech therapy, and respite care. Angels of Care operates in seven states, up from two states prior to their partnership Varsity Healthcare Partners, and employs more than 2,000 nurses, physical therapists, and other service providers.

Nautic Partners, based in Providence, RI, is already a backer of VitalCaring Group, a similar agency with locations across the southern United States, Integrated Home Care Services, providers of DME, home care, and infusion services in Puerto Rico, almost 30 additional healthcare companies. Nautic is a middle-market firm founded in 1986. They specialize in healthcare, industrials, and services.

Partnership

CVS’ Aetna has partnered with Monogram Health to offer in-home care services to Medicare Advantage members with chronic kidney disease. Nurses from Monogram will provide in-home and virtual appointments to eligible members. The two companies will also reportedly work to get timely referrals for kidney transplant evaluations.

Monogram Health is a tech start-up for in-home kidney disease management. Their latest growth funding round garnered $375 million in new funding from health care companies and financial backers, including CVS. Monogram has raised a total of $557 million. Monogram operates by creating value-based care deals with health insurance plans and risk-bearing providers to manage chronic and end-stage renal diseases.

If this model sounds familiar to you, it might be because we wrote last week about Gentiva, which is partnering with risk-based providers to offer palliative care services with risk-sharing benefits on both sides. I expect this is not the last time we will hear/write about risk-sharing partnerships to pay for services that aren’t covered by health care plans.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Kristin Rowan | Feb 7, 2024 | Admin, Marketing, Regulatory

by Kristin Rowan, Editor

Medicare Advantage has multiple measures of success for payment bumps and bonuses. Rehospitalization rates has long been the most important measure of how well a care at home agency is performing, but there are additional measures that can help or hurt your agency. One that is gaining a lot of traction with MA and can impact your agency’s ability to survive is the overall patient experience. Measuring the patient experience can be subjective, but a great marketing tool to use is the Net Promoter Score (NPS). NPS is a calculation of patient responses regarding their likelihood to recommend you to others. A NPS score of “0” means that, overall, your clients are not going to speak positively or negatively about you; there just isn’t anything outstanding enough to bother saying anything. Anything above zero is better than nothing, but 30 and above is ideal.

During January’s HomeCare 100 Winter Conference, Tim Craig moderated the panel, “The MA Member Experience and Why it Matters” with a panel of experts. He posed this question to the audience:

“How well do home care providers perform when it comes to delivering on patient experience?”

Rating care provider performance on a scale of 1-5, the responses during the panel were somewhat surprising

- 47% of those who responded rated the delivery on patient experience 3

- 43% said 4

- 6% responded 2

- A mere 4% responded 5

- There were no responses of 1

If we turn these answers into a Net Promoter Score, we get -6. If caregivers, administrators, and providers don’t believe we’re doing a good job, how can we expect our clients, patients, and families to be happy with the care they receive?

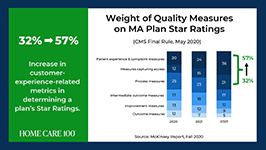

Statistics

- Patient experience and complaint measures count higher toward star rating than they have before

- CAHPS Scores have changed weight from 1.5 to 4 since 2021

- Star Ratings Determine Bonus Eligibility and Amount – starts at 4 stars and above

- Number of plans that have a 4.0 or higher star rating dropped from 64% to 43%

- Disenrollment is on the rise from 10% in 2017 to 17% in 2021

Net Promoter Score

Glen Moller, CEO of Upward Health, whose net promoter score is a whopping 86, said:

“The Member Experience has always been important. What has changed is the way we manage it, given the implication of the CAHPS rating, you can’t be a 4 star without high CAHPS scores.” Moller improved his patient experience with internal surveys to get actionable intel and asking open-ended questions. Look at change and innovation and how that could be disruptive to members. Member experience is at the center of all the other measures. No matter what benefits you’re offering, embed member experience measures at every step of the process.

Because your star rating directly impacts your ability to receive bonuses and because experience-related metrics are increasingly weighted in determining star ratings, you should be looking at the member experience more closely in all of your process. You should also be measuring the member experience and looking at ways to improve it.

Ways to measure ME

• HHCAHPS

• Quality of Patient Care Ratings

• Word of Mouth

• Net Promoter Score

• Glassdoor

• YelpCalculating a Net Promoter Score can be challenging, especially when trying to get older or infirmed patients to answer a survey. For the most accurate NPS, send a single question survey to all of your current and past customers asking them to rate, on a scale of 1 to 10, “How likely are you to recommend us to a friend or family member.” If you aren’t able to do this, you can still calculate a rough NPS using your other measures. You can use your Google and Yelp reviews with a simple formula: % of promoters – % of detractors = NPS. Three stars and below are detractors; four and five stars are promoters.The NPS score is more about comparative to the usual experience rather then the actual experience. A high score from a customer doesn’t necessarily meant it’s “great”, only that it’s much better than what they’re used to or what they expected.

The NPS is not the only measure of customer experience. To get the whole picture, use all the data you have to find out what interventions should be done and implement them. Whether the change is in training your staff, updating your scheduling process, using AI to help communicate directly with patients and families, or simply streamlining your website for a better user experience, you can improve your chances for higher ratings and bigger bonuses in a few easy steps.

I won’t often insert a shameless plug into an article, but if increasing patient satisfaction and member experience can help your agency survive the CMS pay cuts, and you need help with getting a NPS, understanding how to measure your patient experience, or getting online reviews, please contact me for more information. My marketing agency is happy to help get you started.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Elizabeth E. Hogue, Esq. | Feb 7, 2024 | Admin, Regulatory

by Elizabeth E. Hogue, Esq.

A caregiver in Wyoming who is charged with causing the death of her mother has been jailed based on allegations that she committed aggravated assault and battery; deliberate abuse of a vulnerable adult; and intentionally and maliciously killing another human being, commonly known as 2nd degree murder. The defendant, Edwina Leman, cared for her mother, Mary Davis, beginning in June of 2022. At the time of the events described below, Davis was a hospice patient.

On December 28, 2023, Leman’s son heard her yelling at her mother. At some point, he heard an audible “thump” and Davis began to scream. The son then entered the bathroom and found Leman pulling roughly on her mother’s leg, even though Davis was screaming that it hurt. According to Leman’s son, Leman then told her mother “not to be dramatic” and called her “Marygina,” a derogatory name the caregiver had previously called Davis on multiple occasions.

Leman claimed that she was removing her mother’s clothing “more forcibly than necessary when she fell.” She also said that Davis became very frail and fragile during the time the patient lived with her. Leman admitted that she had a temper and had “thumped or swatted” her mother on the head at various times in the past.

Leman’s husband and son said that they saw the caregiver engage in a pattern of physical and verbal abuse toward Davis. The caregiver screamed at her mother and sometimes called her names. Leman’s husband said he saw his wife hit the patient on the head and push her while she was walking with her walker. Leman said that she also pushed Davis when she was not using her walker, which caused her to fall to the ground. The coroner’s report said that Davis died of complications of a displaced fracture of her femur.

A sad story indeed! We read it and weep!

This case is a reminder for all types of providers who render services to patients in their homes to be alert to any signs of abuse or neglect, and to take action to protect patients who are subject to abuse or neglect. Action by providers should include reports to adult protective services. Providers may respond to this recommendation by saying that adult protective services rarely takes action based on their reports. Providers must remember, however, that reports to adult protective services are required in many states. In addition, it is important to establish a record of abuse and neglect even if authorities do not take action. Better to err, if necessary, on the side of protecting patients.

# # #

©2024 Elizabeth E. Hogue, Esq. All rights reserved. No portion of this material may be reproduced in any form without the advance written permission of the author.

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com Reprinted by permission. One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Kristin Rowan | Feb 7, 2024 | Uncategorized

By Kristin Rowan, Editor

Last month, we published an article in partnership with Bob Roth of Cypress HomeCare Solutions in Scottsdale, AZ about paying for long-term care at home. Since then, I have come across some interesting information as we continue to tackle the issue of paying for care that is not reimbursed by the current Medicare/Medicaid system.

Medicare and Medicare Advantage have set pay rates for home health and hospice care. Home Health Value-Based Purchasing (HHVBP), implemented by CMS, was designed to incentivize agencies by paying more for quality care rather than a higher number of services provided. This is similar to giving advances and pay raises based on performance rather than longevity in a job, which I’m all for. However, the HHVBP overlooked palliative care altogether and neither the fee-for-service model nor the HHVBP model includes supportive (read private duty) care at home. Since these services are not reimbursed, there is no incentive to provide them nor way to get paid for them if the patient cannot pay out-of-pocket.

This causes two problems:

1. Home Health and Hospice Agencies are reluctant to provide unreimbursed care, with good reason, so the overall patient experience is less than ideal, rehospitalization rates increase, star-ratings and scores decrease, bonuses go away, and the agencies make less money than before.

2. Patients can’t get the care they need and want. Palliative care patients may receive Hospice care too early, or they may not receive care at all because they fall between home health and hospice. Patients who need supportive care at home can’t afford it so they either go without, causing increased complications or they rely on friends and family members who burn out under the stress of being a full-time caregiver.

Innovative care strategies can overcome the obstacles faced by agencies and patients alike. There may not yet be a perfect solution, but there are some innovative ideas out there and something has to disrupt the current pay model.

Palliative Care Partners

Medicare Advantage organizations and primary physician groups receive a “cost of care” analysis for the duration of the patient care. The organization takes on the risk of that patient costing more than what the MA plan will pay, but can make more money if patient care costs less than anticipated. Palliative care at home costs less. David Causby, President and CEO of Gentiva, a Hospice organization that operates in 35 states across the U.S. and has an average daily census of 26,000, has implemented a plan of care in cooperation with these organizations in what he calls Advanced Illness Management (AIM) Model for Risk-Based Partnerships. Designed for palliative care, Gentiva creates a plan of care that includes visit frequency and care needs and employs nurse practitioners, care managers, after hours RNs and social workers. The hospital pays Gentiva on a PMPM model with shared savings. The hospital still gets paid the full amount from MA but uses fewer resources, has lower costs, and sees reduced rehospitalizations, saving more than what they pay out. According to Gentiva, this partnership “provides value to contracted organizations by decreasing the overall end-of-life spend on this high-risk patient population.”

Supportive Care at Home Innovations

Supportive Care at Home (Private Duty Home Care, Private Pay, Non-medical home care) is not covered by Medicare, Medicare Advantage, or most health insurance plans. Limited Medicaid grants, VA plans, and long-term health insurance pay for some supportive care at home. Without one of these plans, patients and family members pay out-of-pocket for supportive care at home, averaging $22-$27 per hour with a 4-hour minimum. In some states it can cost up to $50 per hour. At $80 per day, that’s around $20,000 per year.

One software company we recently spoke with is upending the home care model with fee-for-service model that charges by the minute, rather than by the hour, making care more affordable for more people. You can see our product review of Caring on Demand here. By reducing the cost for customers and reducing the time for caregivers, agencies can onboard more customers without hiring more caregivers. The system is being used in facilities where these services are not provided, which allows a caregiver to visit several people in one stop. The agency and the caregiver can see the same income in the same time, spread out across multiple private payers.

Combining Innovation for a Win-Win-Win

I heard about Caring on Demand and spoke with its founder in August of 2023. I spoke with one Home Care agency owner who recently started working with Caring on Demand. “Times have changed,” the agency owner said. With fewer caregivers joining the workforce, increased levels of burnout since 2020, and CMS changes that overlook palliative and non-medical care, maybe there’s another way…

- Partnerships with organizations and physician groups that have Medicare, MA, and traditional health insurance patients, non-medical home care agencies, and palliative care providers.

- Localized groups of patients in limited areas like retirement villages, planned communities, neighborhoods, or small towns.

- Cost sharing and care coordination that includes in-home palliative care visits, supportive care, communication with primary care providers and specialists

- Preventative intercessions to avoid unnecessary ER visits and hospitalizations

- Shorter visits per caregiver with multiple visits to a community each day

- Cost sharing among patients splitting a 4-hour minimum visit among 4-8 patients

- Shared savings from reduced hospital stays, shorter durations of hospice care, and nursing visits that are supplemented by supportive care

Gentiva has experienced some success already in using shared savings as a payment model. Can costs be decreased even more by adding supportive home care to this plan? Is there enough shared savings for three payees instead of two? I don’t have the answers to these questions, but I do believe providers of supportive care and palliative care have been in the background, overlooked by CMS and MedPAC for long enough. If they aren’t going to recognize the positive impact and cost savings of home care and palliative care and include them in the reimbursement model, we may have to do it for them.

We’d love to hear your feedback on this and other innovative ways to combat the crisis of paying for care at home.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Rowan Report | Feb 7, 2024 | Admin, Recruitment & Retention

by Jen Waldron,

Recruiting caregivers for your home care agency franchise can be challenging enough, but it’s even more frustrating when those same caregivers don’t bother to pick up the phone after applying for your jobs. You may have put in a significant amount of time, money, and energy into trying to find qualified caregiver applicants, only to be repeatedly met with radio silence, missed calls, or unanswered texts.

In my mission to help home care agencies recruit more efficiently, I have identified the top five reasons why caregivers do not pick up your calls and what you can do about it.

1. You are not offering competitive pay or benefits

In a comprehensive study Pew Research found that the number one reason people leave their job is, in fact, for more money. But the number two and three reasons are “no advancement opportunities” and “feeling disrespected at work.” If your compensation package — and your career advancement opportunities — are not competitive, caregivers may choose to ignore your calls and continue searching for better opportunities.

2. Your job ad looks like spam; your hiring process does not stand out from the crowd

Candidates do not read your job description, especially if it is wordy. All job posts look like spam to the applicant, they apply to too many jobs, as many as 16 or more at one time!, and, as a result, they never read job descriptions.

This confusion can lead to candidates feeling apprehensive about texts and phone calls from unknown numbers and explain why they often opt not to answer your phone calls. The screen shot below is an example of how caregiver applicants get too many messages about jobs. To stand out from the crowd, an agency HR team must find a different way to communicate with the applicant about the value and challenges of your jobs.

3. You are not demonstrating professionalism in your hiring process

Caregivers are professionals and they expect you to have a professional hiring process. Many agencies use hiring software built for other industries and, as a result, their hiring process is clunky. On many job boards, applicants “1-click” apply with a job seeker profile they may have made several years ago. When they are followed up with through some sort of automated text system (which they think looks spammy – see pic!), they are annoyed that they are being asked to “apply” again.

4. You have poor online reviews or ratings

Today, people trust online reviews and ratings as much as personal recommendations from friends or family. If your agency has too few positive or too many poor online reviews from clients and/or employees, caregivers may not have confidence in you as an employer. Even if the impression they glean from your reviews is inaccurate, they may choose a competitor whose reviews reflect the culture and work ethic more suitable to their own. Therefore, it is imperative that you invite positive feedback from satisfied clients and employees and respond quickly to negative online reviews. This is critically important to attracting caregivers interested in working for you.

5. Your recruitment process takes too long; caregivers are moving on

The data shows that 57% of applicants today expect to hear back about the position they applied for within 1 week. With regard to retention after onboarding, one of the reasons caregivers leave is they are not given enough hours to make full time work. They say they want those hours to be in the right location and compatible with their scheduling needs and experience level.

You do not want to incur the cost of going through the whole interview, orientation, and hiring process if you do not have the right clients to match their needs and preferences at that time. Therefore, it is vital to streamline your recruitment process and to implement fast and efficient process with the best applicants.

In Summary

As a home care agency owner, it is essential to understand why caregivers may not answer your calls, even after applying for your jobs. Based on our five reasons applicants do not pick up your calls after they apply, there are steps you can take to improve your odds of attracting the best applicants:

-

- Evaluate your recruitment process, compensation package, job description, communication methods, and online reputation.

- Ensure you demonstrate professionalism through your interactions, online and during interviews.

- Make your job description and requirements stand out amongst the spammy looking emails and texts out there today.

- Take steps to eliminate bottlenecks in your hiring process.

By doing so, you will attract the best caregivers who will choose to work with you, and your agency can grow and thrive.

# # #

Jen Waldron is one of the co-founders of Augusta Home Care Recruiting She started working in the senior care industry in 2009 as a professional caregiver in a memory care community. Since then, she has been an executive supporting thousands of home care agencies and other senior care businesses through software solutions. Augusta is an innovative software company designed entirely for home care. The platform gets caregivers to show up to interviews through inspiring confidence in the applicant, speed to hire and identifying top talent.

Jen Waldron is one of the co-founders of Augusta Home Care Recruiting She started working in the senior care industry in 2009 as a professional caregiver in a memory care community. Since then, she has been an executive supporting thousands of home care agencies and other senior care businesses through software solutions. Augusta is an innovative software company designed entirely for home care. The platform gets caregivers to show up to interviews through inspiring confidence in the applicant, speed to hire and identifying top talent.

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Kristin Rowan | Feb 7, 2024 | Regulatory

by Kristin Rowan, Editor,

On Wednesday, January 31, Cigna and HCSC signed an agreement to sell all of Cigna’s Medicare business — including traditional Medicare, supplemental benefits, Medicare Part D offerings, and CareAllies, a value-based care management subsidiary. — to HCSC, a Blue Cross / Blue Shield partner with operations in Illinois, Texas, New Mexico, Oklahoma and Montana. The $3.3 billion deal will quadruple the size of HCSC’s Medicare Advantage population, which numbered 217,623 as of this month.

Medicare Advantage had not been a significant business for Cigna. CEO David Cordani explained that it required resources disproportionate to its size in the company. With 19 million insurance customers, Cigna had a little over a half million in its MA business, a little under a half million Medicare supplement members, and 2.5 million in Part D.

It had previously been reported that Cigna believed divesting its Medicare business would make its merger with Humana more acceptable to regulators. The company completed its HCSC deal even though negotiations with Humana had already broken down. Though inked today, the deal is not expected to close until the first quarter of 2025.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

by Tim Rowan | Feb 7, 2024 | Admin, Vendor Watch

by Tim Rowan, Editor Emeritus,

Advertising in The Rowan Report comes with a few perks! Our CEO interview with Tim is one of them. Advertisers with a full-year contract receive one annual CEO interview with Tim. If you’re not an advertiser, CEO interviews can be purchased as well. Highlight the expertise of your leadership with a one-on-one industry overview and company update with Tim, published on The Rowan Report website, social media, and YouTube channel.

Click on these titles to view each episode of our “Meet the CEO” video interview series.

Andre Gomez, Bedrock Healthcare at Home, January 2024

Rich Berner, Complia Health, December, 2022

Emmet O’Gara, Sandata, September, 2022

Roger Shindell, Carosh Compliance Solutions, June, 2022. HIPAA risk assessment workshops

Michael Gelman, CareConnect, May, 2022, Workforce Management

Jim Bland, Seniors Home Services, November, 2021, A menu of products from remote patient monitoring to home modifications, all with revenue sharing for home care partners

Ashley Wharton and Jenna Schwartz, Savii, March, 2021, Private Duty Agency Management Software

Eric Becker, CEO, MiliMatch, on technology to improve recruiting and retention

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim Rowan is a 30-year home care technology consultant who co-founded and served as Editor and principal writer of this publication for 25 years. He continues to occasionally contribute news and analysis articles under The Rowan Report’s new ownership. He also continues to work part-time as a Home Care recruiting and retention consultant. More information: RowanResources.com

Tim@RowanResources.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report.homecaretechreport.com One copy may be printed for personal use: further reproduction by permission only. editor@homecaretechreport.com

© 2024. All content is produced by The Rowan Report. All rights reserved.

by Kristin Rowan | Jan 31, 2024 | Clinical

By Kristin Rowan, Editor

The National Association for Home Care and Hospice joined other advocacy groups this month on Capitol Hill to fight against the looming pay cuts from CMS. Some members of Congress joined the fight for “common sense policies” to expand access to care in the home for Americans.

Rep. Adrian Smith (R-NE-3), who spoke at the event, decried moves against home health, saying “there are cuts looming that are not based on reality” and “we want to make sure reimbursement policies are reflective of the actual realities.” Smith is also the representative who introduce the “Homecare for Seniors Act,” H.R. 1795, which would allow the use of Health Savings Accounts (HSAs) to be used for home care.

Rep. Terri Sewell (D-AL-7) has a personal connection to home care and spoke about how her mother cared for her father through a series of strokes he suffered. She expressed strong opinions about payment reductions that could see home health lose as much as $20 billion dollars over the next ten years. Sewell called the idea “frightening” and said, “I am a big fan of making sure that my constituents have access to quality, affordable health care.”

The Medicare program has admitted that home health is not just a bringing of great care and not just a more cost effective way to provide care, but is a service that provides dynamic value. Care in the home has decreased overall costs by $3.2 billion dollars just in the small segment of value-based payment model test cases. Patients who receive care in the home are re-admitted to the hospital 37% less frequently than those who do not and are 43% less likely to die than patients who do not receive care at home. Still, CMS is looking at additional pay cuts which bring the total payment reduction down 13.72% since 2019. The costs of everything else have increased in that time. According to the U.S. Bureau of Labor and Statistics, the average cost of living has increased 22% since 2019. NAHC President Bill Dombi said, “Where we’re headed in 2024 is that half of all home health agencies will be operating in the red with the cuts facing them in the Medicare program. It’s not a recipe for continued access to care.”

Dombi, along with many others, is predicting that 50 percent of agencies will be operating in the red after the next round of payment reductions and that without a reversal of these pay cuts we could see the end of care at home altogether with a collapse of the home health payment system.

The advocacy event on Capitol Hill helped raise awareness of the plight of care at home among some policymakers, but more help and advocacy is needed. Please, take a few minutes to click the link below and tell your members of Congress to support the Preserving Access to Home Health Act of 2023.

# # #

Kristin Rowan has been working at Healthcare at Home: The Rowan Report since 2008. She has a master’s degree in business administration and marketing and runs Girard Marketing Group, a multi-faceted boutique marketing firm specializing in event planning, sales, and marketing strategy. She has recently taken on the role of Editor of The Rowan Report and will add her voice to current Home Care topics as well as marketing tips for home care agencies. Connect with Kristin directly kristin@girardmarketinggroup.com or www.girardmarketinggroup.com

©2024 by The Rowan Report, Peoria, AZ. All rights reserved. This article originally appeared in Healthcare at Home: The Rowan Report. One copy may be printed for personal use: further reproduction by permission only. editor@therowanreport.com

- Please GO HERE to tell your members of Congress to support the Preserving Access to Home Health Act of 2023

by Elizabeth E. Hogue, Esq. | Jan 31, 2024 | Admin, Regulatory

by Elizabeth E Hogue, Esq.

Providers may have heard or read about the importance of Fraud and Abuse Compliance Plans in their organizations. Despite the wealth of available information about Compliance Plans, many providers continue to express uncertainty about their value. Here are some of the questions providers commonly ask about Compliance Plans:

Why should we have a Fraud and Abuse Compliance Plan?

First, the Office of Inspector General (OIG) of the U.S. Department of Health and Human Services has clearly stated that, consistent with the Affordable Care Act (ACA) as described below, all providers are now expected to have current Compliance Plans that are fully implemented.

As a practical matter, when providers establish and maintain Compliance Plans, it clearly discourages regulators from pursuing allegations of fraud and abuse violations.

Technically speaking, the Federal Sentencing Guidelines make it clear that establishment and implementation of Compliance Plans is considered to be a mitigating factor. That is, if accusations of criminal conduct are made, the consequences may be substantially less severe because of a properly implemented Compliance Plan.

In addition, providers with Compliance Plans are more likely to avoid fraud and abuse. This is because Plans routinely establish an obligation on the part of every employee to report possible instances of fraud and abuse, and Plans include training for all employees.

Compliance Plans may help to prevent qui tam or so-called “whistleblower” lawsuits by private individuals, rather than by government enforcers, who believe that they have identified instances of fraud and abuse. There are significant incentives to bring these legal actions since whistleblowers receive a share of monies recovered because of their efforts. Some whistleblowers have received millions of dollars. Compliance Plans make it clear that employees have an obligation to bring any potential fraud and abuse issues to the attention of their employers first. Compliance Plans provide a clear path to resolve fraud and abuse issues internally.

In addition, the federal Affordable Care Act (ACA) requires providers to have Compliance Plans. In short, it’s the law!

Finally, the Deficit Reduction Act (DRA) requires providers who receive more than $5 million in monies from state Medicaid Programs per year to implement policies and procedures, provide education to employees, and put information in their employee handbooks about fraud and abuse compliance. These requirements can be met through implementation of Fraud and Abuse Compliance Plans.

We don’t receive reimbursement from the Medicare or Medicaid Programs. Do we still need a Compliance Plan?

Statutes and regulations governing fraud and abuse also apply to providers who receive payments from any federal and state healthcare programs, including Medicaid, Medicaid waiver and other federal and state health care programs, such as TriCare and the VA. Many private insurers have followed the federal government’s lead in terms of fraud and abuse enforcement. Therefore, providers that don’t receive reimbursement from the Medicare Program must have compliance plans, too.

We hear that the OIG of the U.S. Department for Health and Human Services has provided guidance for various segments of the healthcare industry regarding Compliance Plans.

- Specifically, the OIG has already published guidance for clinical laboratories, hospitals, home health agencies, hospices, physicians’ practices, third-party billing companies, and home medical equipment companies. Should we just use the model guidance that is applicable to us?

The answer is, “No!” Guidance from the OIG is not a model Compliance Plan. Guidance from the OIG consists of general guidelines and does not constitute valid Compliance Plans. In addition, the OIG has made it clear that Plans must be customized for each organization.

We have read that, before implementing Compliance Plans, providers must conduct expensive internal audits that can take many months to complete. Is this true?

While beginning the compliance process with an extensive internal audit is certainly one way to proceed, it is not the only viable way to work toward compliance. It is equally valid to begin with Compliance Plans that are customized for the organization and include training for all employees about fraud and abuse, and Compliance Plans. Then all staff members can subsequently participate in internal compliance activities, including audits, with a process in place to handle any issues that arise as a result of the audits.

We have all sorts of policies and procedures in our organization. Why do we need something else called a Compliance Plan?

Compliance Plans are specific types of documents that routinely address fraud and abuse issues that providers do not usually cover in internal policies and procedures. In addition, providers may not gain benefits under the Federal Sentencing Guidelines described in paragraph one (1) above if there is no formal document called a Compliance Plan.

We just spent a lot of money to become accredited or reaccredited. Doesn’t certification mean that we are in compliance?

On the contrary, Compliance Plans appropriately address potential fraud and abuse issues. They also include mechanisms for helping to ensure compliance, such as processes for identification and correction of potential problems that are not addressed during the certification process. In other words, organizations may be accredited, but fail to meet applicable compliance standards for fraud and abuse.

Will the fact that our organization has a Compliance Plan make any difference regarding the outcome of fraud and abuse investigations and the imposition of Corporate Integrity Agreements (CIA’s)?

Yes, it may make a considerable difference, based on statements from the OIG. If providers have Compliance Plans in place during investigations that are current and fully implemented, the OIG may be less aggressive in pursuing potential violations. Enforcers are likely to ask for information about Compliance Plans and related policies and procedures. Enforcers are now also likely to ask providers to show them how much money they have spent on fraud and abuse compliance activities!

When the OIG discovers problems with fraud and abuse in organizations, providers are usually asked to develop and implement a Corporate Integrity Agreement (CIA). The OIG often requires CIA’s to include a process for stringent monitoring by the OIG on a continuous basis. These monitoring activities can be extremely burdensome to providers in terms of both time and money. Providers with valid Compliance Plans may not be asked to develop and implement CIA’s.

Now is the time for all providers to recognize and act upon the need to establish and maintain Compliance Plans. “Working on it” is no longer good enough.

©2024 Elizabeth E. Hogue, Esq. All rights reserved.

No portion of this material may be reproduced in any form without the advance written permission of the author.